Risk Vs Safety: What Diversification REALLY Means

Apr 06, 2022

Don't put all your eggs in one basket!

It's an oldie but goodie. There's a lot of phrases out there that are just oldie... outdated... and terrifyingly irrelevant, but people still listen to them. Yikes! 😳😬😖

But the message about diversifying is as relevant and true as ever. And as we like to say at Smart Money Works... Diversification doesn't mean that you own stock in both Apple AND Microsoft 😆

Here's a great way to think about diversification: think about the balance between your Risky Money and your Safe Money.

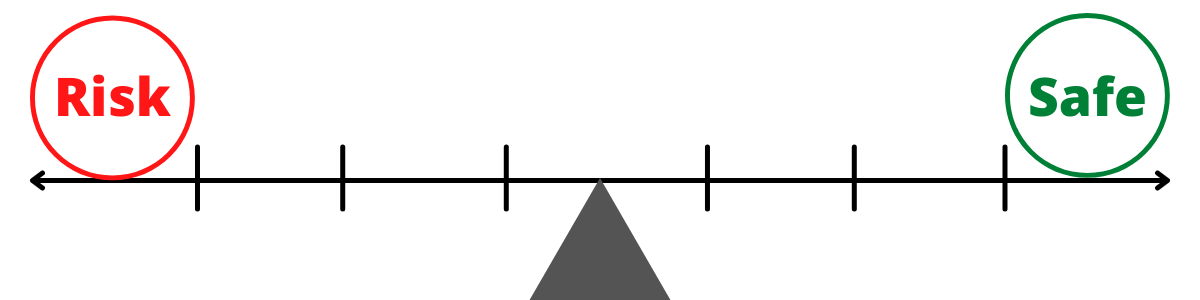

Risk Vs. Safety

Here is the Risk versus Safety teeter totter. Each kind of asset you have is somewhere along this scale.

What people like about Risky Money is: that's where we can see big gains 😁 but we can also suffer big losses 😭

We like Safe Money because we can't lose money in those assets 😅 but we don't usually see a lot of growth there 😕

Here's where it gets interesting: Most of us have been taught (if we're lucky) that stocks are risky; mutual funds are safer; and bonds are really safe.

Au contraire, my friend! There are 12 or 13 different types of assets (we've broken them down into different blog posts here, here, and here)- there are way more asset classes than just stocks, bonds, and mutual funds 🤯

Thinking about the big picture, assets like cryptocurrency are way on the outside edge of risk, practically off the teeter totter altogether. Commodities and futures are highly risky; stocks slightly less so. Mutual funds are slightly safer than that, and bonds are slightly safer than mutual funds- but even bonds are still on the Risky side of the teeter totter.

What about real estate? There's still some risk there- while real estate value goes up reliably, outside factors can negatively affect your gains- a bad renter defaults, expensive repairs are required, etc 🏡

What Assets Are On the Safety Side?

There are fewer types of assets to balance out the Risky side of the teeter totter here; but they do their job perfectly well- making sure you don't lose money.

Remember: every time you lose money you have to make up for your losses before you are actually making money. In other words, you have to make money to get back to square one; then you start growing your wealth again.

So what safe assets balance out your risky assets? A checking/savings account, money market account, or CDs all fall into the Safe category.

Unfortunately, those accounts usually don't make any money for you; they don't grow your wealth. And if those assets grow at all, they never keep up with inflation 😖

Fortunately, there is one type of asset on the Safe side of things that actually grows well- in addition, it grows tax-free AND is distributed tax-free. This asset is called a tax-free indexed account 💲

Indexed Accounts

How It Works: You put money into this asset, and it is held safe in your account; just like a savings account. But every year, your account gets credited with interest, and the amount of interest tracks the index of the stock market.

Interesting side note: Stocks and mutual funds never grow on track with any stock market index. Out of all the hedge funds that exist, only about a half a dozen actually track or outperform the stock market in any given year. Fascinating! 🤔

Back to indexed accounts: They always track the stock market index, but they are Safe Money assets, so you can never lose money in them. So, for example, let's say the stock market grows at 8% over the last year; well, then your indexed account is credited with 8% growth 📈

Let's say the next year, the stock market drops by 10%. Your indexed account is protected against losses, so you are credited with 0% for that year.

Now, are you upset that you get credited with 0%? In this case- absolutely not! All your friends have lost 10% in the market, and you haven't. That's when zero becomes your hero 🤩

Too good to be true?

Never!

And here's why: Let's sat that, the following year, the stock market has rebounded (we always have our biggest gains after years with the biggest losses.) The stock market earns 13%- nice!

But here's where an indexed account is not too good to be true- your indexed account is subject to a cap on growth. Let's say that cap is 9%- when your friends are over there earning 13%, your account will be credited with 9%.

The caps on growth are how an indexed account can both protect you against losses, and still grow by tracking the stock market.

Realized Vs Unrealized Gains

An important thing to note here is that all gains in an indexed account are realized gains. This means that when you are credited with gains, that credit remains yours, forever, so you can never lose your principal OR your gains.

The way it works in capital assets (like real estate) or the stock market is that you have "unrealized gains" until you sell your asset. An unrealized gain is your increase in value of an asset you haven't yet sold.

In other words: when you look at the account value in your indexed account- that is how much money you have. When you look at the account value in your brokerage account or 401k or the value of your real estate, that is how much money you would have- could have- might have- if you sold your asset right then; but you have to sell that asset first 🤝

So there's an advantage of certainty in the indexed accounts, and not feeling like you have to "time the market"- which is darn near impossible 🦄

What Diversification REALLY Means

We've set the stage on discussing what are risky assets, and what are safe assets.

Diversification means that you have some of your money in several different types of assets. You will protect yourself against any downsides of those assets, and take advantage of all possible upsides of your assets.

In America, we make the mistake of thinking, "if a little is good, isn't more better?" Not at all. A little sugar is delicious- a lot will give you diabetes. Speeding in your car a little will get you to your destination faster- speeding a lot is dangerous.

We all know that balance is best in so many arenas in life- this applies to our wealth, as well. Balance in your wealth means that you spread the risk out by having lots of different types of assets under your financial umbrella.

How Does It Work?

Most of us are overbalanced in owning mostly Risky Money, because we aren't aware of the other options available to us. Here's how to apply the Risk Vs. Safety teeter totter to your own assets:

- Draw out your own Risk Vs Safety teeter totter on a sheet of paper.

- What types of assets do you have? Write them down, about where they'd be on the Risk Vs Safety scale.

- Shift your balance point.

Are you more comfortable with risk? You might be more comfortable with risk if you are younger, male, and/or wealthier. Erase your balance point (the triangle under your teeter totter) and shift if to the left if you like risk.

Do you prefer safe money? You might desire safety more if you are older; female; or if you or a family member suffers from an illness/injury/disability. You might also be risk-averse/safety-oriented if you are just starting out, less affluent, and just can't afford to lose anything. If this is you, erase your balance point and shift if to the right if you prefer safety.

And of course, your own personality plays into this. TBH... more people desire safety than are comfortable with risk, so if that's you, welcome to the club! - Make sure you have equal amounts of money on each side of your teeter-totter with its new, customized balance point. Not balanced yet? Shift money between assets with the help of your financial professionals; or, when you add more money to your long-term savings, make sure you are adding money to the assets in the desired part of your teeter-totter.

- Have fun! Whew, doesn't it feel better now that you have several different kinds of assets? And that your assets are balanced the way that makes YOU feel comfortable? It gets really exciting to watch your wealth grow when it's aligned to your preferences.

Now That's Smart Money 🧐

Isn't this content awesome?!

...Want more FREE content?

Just sign up for our FOREVER FREE email course &

get fantastic info, insight, and ideas-

delivered directly to your inbox. Sign up today- it's easy!

We hate SPAM. We will never sell your information, for any reason.