Your Financial House Is Now 2nd Level

Aug 21, 2020

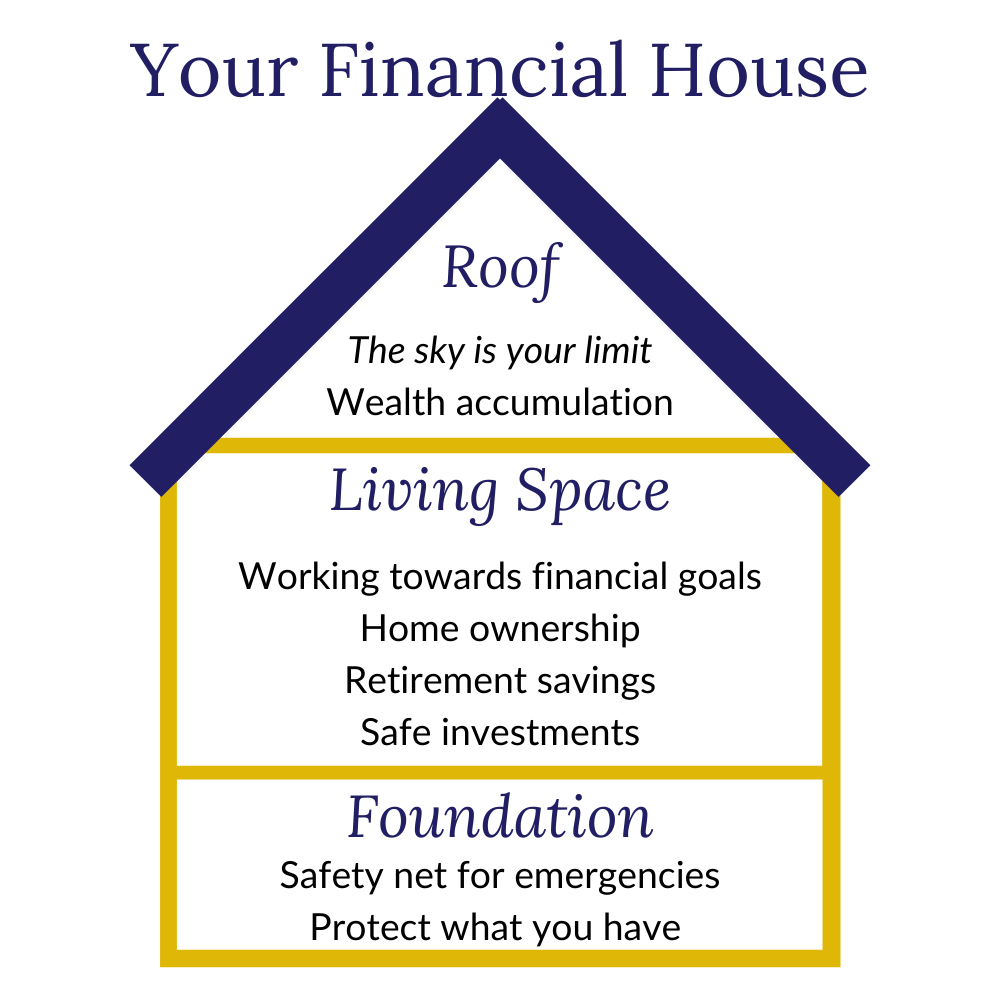

A few weeks ago we talked about the most important part of your financial house- your foundation. It’s the basis for, and the most critical piece of, your financial house- but wait, there’s more!

Your financial foundation is how you protect yourself, your family, and your assets. After all, why build something up, if it can all disappear at the first sign of trouble? And, knowing that you have a safety net and the protection you need, you will have the peace of mind to confidently make good financial decisions moving forward 😃

You’ll never need to worry that the unexpected will sideline you from your financial goals for an undetermined length of time 😬

So, once those pieces are in place, you can move on to building the fun parts of your financial house! In gamer-speak, you have “leveled up” 🎮

Now you’re ready to work on the 2nd level of your financial house. These are the parts of your house that you “live” in- the financial plan that you’re regularly following, in your day-to-day living. It’s a lot like the house-buying process, actually- you have to do the boring parts like an inspection and lots of paperwork, but once the house is yours, you get to buy new furniture, paint walls, do whatever will make your new house feel like your home 😁

When it comes to your financial house, the fun parts are figuring out what you want and how you’ll get there! 😊

Everyone has different financial goals. Building wealth, saving for children’s futures, owning a home, and retiring at a specific age are extremely common goals, but there are also other goals. Some people create plans for charitable giving or leaving a legacy; other people create smaller, more achievable goals that change once each goal is met 👶🏠👴🏼💲

Building the “living space” of your financial house is just the process of creating a plan that meets your goals- and following it! It’s a little difficult to give general advice here, when each person’s plan is different in its goals and in its execution, but following are some general principles.

Homeownership is a great topic, because it’s salient to a great number of financial goals like retirement goals, wealth building, leaving a legacy, or simply homeownership itself. Owning a home is one of the top two ways to build wealth, so it’s great to understand the financial impact of owning a home 💸

I’m a numbers geek, so I find these numbers really interesting: over a 15-year period (from 1999-2013), those who remained homeowners increased their average wealth by $92,000. People who went from renting to owning increased their wealth by $85,000 😁

People who went from owning to renting (Thanks, Great Recession ) saw a $48,000 decrease in wealth 😪

Let’s rephrase: How long would it take you to save $85,000? Or $92,000? You can get that in 15 years, just by paying a mortgage 🤯

Homeownership isn’t for everyone; if you will not or cannot care for a piece of real estate, then definitely keep renting. And yes- saving up for a down payment is the worst, especially if you’re paying high rent already. It can be hard- really, really hard- to become a homeowner. We’ll talk more about homeownership in a future Smart Money Minute 🏠

But owning a house makes it much easier to build your financial house! 🏡

The second-best way to build wealth is to save for retirement. The key to that is the power of compound interest- earning interest over time can have a huge impact on your overall wealth 📈

And when we are talking about the middle of our financial house- the “living space”- it’s often best to start by using safe investments.

The concept of risk vs. safety is more conversation-worthy than you think. Everyone has different levels of risk avoidance/risk tolerance. Most couples do not have the same level of risk tolerance between partners, so how do you choose whose risk tolerance to follow? If it’s not something you and your partner can agree on, it’s often best to ask a financial professional for help in setting goals and building a plan 😄

So, the concept of “safe” investments could actually vary by person! Historically, safe investments included vehicles like money market accounts, CDs, and bonds.

We can consider those vehicles safe, but I wouldn’t call them investments! Investments are supposed to earn you money over time; but the interest rates on money market accounts, CDs, and bonds are so low that they don’t have a lot of value. Consider that inflation hovers just under 3% per year; that means that you have to earn at least 3% per year on average, or your money is losing value over time 📉

Safe investments, therefore, should be able to earn enough that your money is working for you, but you won’t lose your shirt if the economy goes south for a few years. These types of accounts are the perfect balance between risk- with its potential for growth- and safety- with its guaranteed protection against loss ⚖️

These are my favorite types of investments, actually. And remember, you shouldn’t put all your money into safe investments- just the money that you can’t afford to/don’t want to lose! 🤣

Once you’ve built the Living Space portion of your financial house, you’ll be ready for the roof! That’s our next topic 👍

Follow your financial plan in your day-to-day living, in order to build up your financial future in the same way that you build a house 🏡

Now That’s Smart Money 🧐

Isn't this content awesome?!

...Want more FREE content?

Just sign up for our FOREVER FREE email course &

get fantastic info, insight, and ideas-

delivered directly to your inbox. Sign up today- it's easy!

We hate SPAM. We will never sell your information, for any reason.